On this page · 11 sections

- What the WSJ actually reported

- Why now — the competitive numbers behind the cuts

- Comparison table — current API pricing across the frontier (June 2026)

- What "drastic" might actually look like

- The IPO context — why this matters now

- What enterprise buyers should expect over the next 60-90 days

- What founders and growth-stage AI companies should expect

- India-specific considerations

- FAQ

- How eCorpIT can help

- References

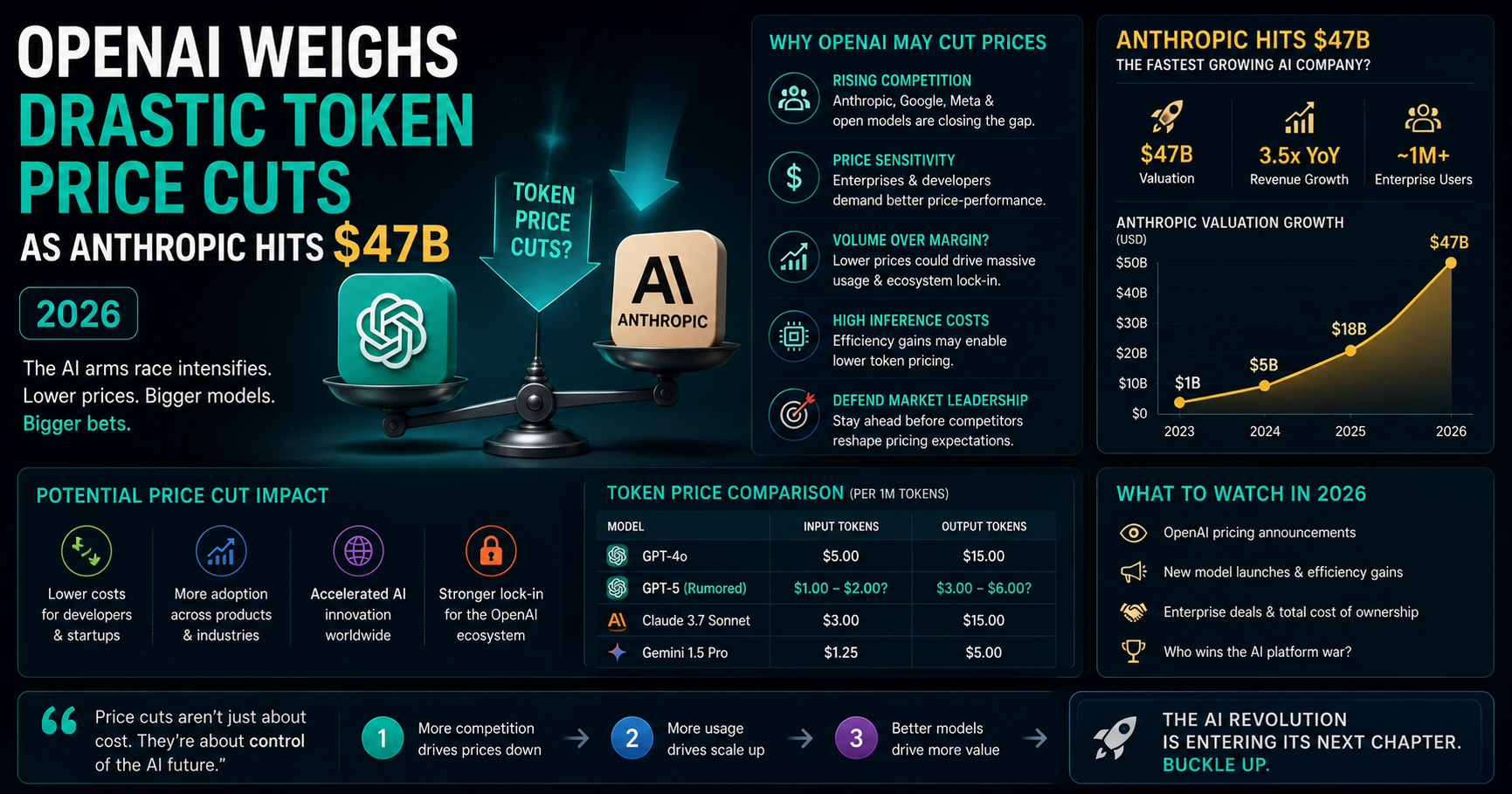

Summary. OpenAI is weighing drastic cuts to its token prices to win customers from Anthropic, the Wall Street Journal reported on Wednesday, June 11, 2026 (Reuters carried the same story). The backdrop is brutal — Anthropic's annualised revenue went from approximately $1 billion in January 2025 to $47 billion in May 2026, a roughly 30x climb in fifteen months, while OpenAI moved from $13 billion to $24-25 billion in the same window. Enterprise market share has flipped: Anthropic now holds approximately 32-40% of enterprise LLM spend depending on the survey, against OpenAI at 25-27% (down from 50% in 2023). The Ramp AI Index for May 2026 puts Anthropic at 34.4% of business adoption against OpenAI's 32.3% — the first time Anthropic has led on that survey. Anthropic launched Claude Fable 5 on June 9 at $10/$50 per million tokens (half the price of Mythos Preview) with an 80.3% SWE-Bench Pro score against GPT-5.5's 58.6% — a 22-point lead two days before the OpenAI price-cut story broke. Sam Altman has reportedly told staff OpenAI plans to file publicly within a year; the company confidentially filed for an IPO this week. Both companies are heading to public markets with their pricing models under pressure. This article covers the WSJ story, the competitive numbers behind it, three comparison tables (revenue trajectory, market share, current pricing), what an actual price cut would look like, and what enterprise buyers, founders and Indian businesses should plan around.

The honest reading: OpenAI is responding to a market position it lost. The story is not "OpenAI is generous"; it is "OpenAI is trying to retain enterprise revenue before its IPO roadshow." Both interpretations matter and both shape what to expect over the next 60-90 days.

This guide is built for AI engineering leaders, CTOs, product teams making model-selection decisions, finance teams modeling AI spend, and business leaders watching the competitive dynamics ahead of two of the largest tech IPOs of 2026-27. Research draws on the WSJ original report, Reuters' syndication, Anthropic's Fable 5 announcement, Ramp's AI Index, and verified revenue data from multiple secondary sources.

What the WSJ actually reported

The Wall Street Journal reported on Wednesday, June 11, 2026 that OpenAI is "weighing drastic cuts" to the prices it charges for AI tokens, anticipating that Anthropic will make similar moves. Reuters carried the same report. Key points from the coverage at Yahoo Finance, US News, MarketScreener and InvestingLive:

- OpenAI is "considering drastic price cuts" as it seeks to "win customers from competitor Anthropic"

- The cuts would specifically target tokens — the central billing unit for AI APIs

- The discussions are described as "still in flux" — no specific numbers or timing have been published

- Sam Altman recently said publicly that "costs had become a huge issue" for business buyers and that the company expects to find ways to help customers "get more value for less spend"

- A price war would test both companies' business models ahead of expected public listings

- OpenAI confidentially filed for an IPO this week; Altman has reportedly told staff the company plans to go public within the next year

- Anthropic is also moving toward IPO — reports suggest an October 2026 timeline as the most cited target

What was not in the WSJ report: specific cut amounts, specific model targets (GPT-5? GPT-5.5? both?), or specific timing. The story is positioned as forward-looking — what OpenAI is "weighing" — rather than a fait accompli.

Why now — the competitive numbers behind the cuts

OpenAI's revenue position is strong in absolute terms but compressed relative to Anthropic. Five data points frame the strategic context.

Revenue trajectory comparison

| Period | OpenAI annualized | Anthropic annualized | Anthropic growth multiplier |

|---|---|---|---|

| January 2025 | ~$13 billion | ~$1 billion | 1x baseline |

| Late 2025 | ~$20 billion | ~$9 billion | 9x in 12 months |

| April 2026 | ~$25 billion | ~$30 billion | 30x in 15 months |

| May 2026 (most recent) | ~$24 billion (confirmed $2B/month run rate) | ~$47 billion | ~47x from base |

Anthropic's growth dynamic — from $1B to $47B in 15 months — is unprecedented in enterprise software history. OpenAI's growth, while strong in absolute terms, lags meaningfully on percentage. The composition of the two revenue lines also matters: Anthropic's revenue is overwhelmingly enterprise; OpenAI's revenue mix leans heavily toward consumer ChatGPT subscriptions (Jefferies estimates over 900 million weekly active ChatGPT users) and a smaller enterprise API business.

Enterprise market share — the strategic battleground

| Metric | OpenAI | Anthropic |

|---|---|---|

| Enterprise LLM spend share (Menlo Ventures cohort, 2026) | ~25% | ~32% |

| Enterprise LLM spend share (alternative survey) | ~27% | ~40% |

| Business adoption — Ramp AI Index May 2026 | 32.3% (-2.9% MoM) | 34.4% (+3.8% MoM) |

| Enterprise customers spending >$1M/year | n/a publicly | 1,000+ (doubled in 2 months) |

| AI programming tool share (Claude Code) | n/a | 54% ($2.5B+ annual revenue) |

The Ramp AI Index May 2026 release is the most cited single data point — Anthropic adoption rose 3.8 points to 34.4%, OpenAI fell 2.9 points to 32.3%. This is the first time Anthropic has led that index. Combined with the 1,000+ enterprise accounts spending over $1 million per year on Claude (a number that doubled in the two months following Anthropic's Series G announcement in February 2026), the enterprise migration story is operationally real.

What pushed enterprises toward Anthropic

Three discrete moves in the past 60 days accelerated the shift:

- Claude Opus 4.8 took the AGI Ranker coding throne at 81.01 versus GPT-5.5's 77.48 in late spring 2026.

- Anthropic launched Claude Fable 5 + Mythos 5 on June 9, 2026 at $10/$50 per million tokens (less than half the price of Mythos Preview). Fable 5 posted 80.3% on SWE-Bench Pro against GPT-5.5's 58.6% — a 22-point lead. eCorpIT covered the launch in its Claude Fable 5 + Mythos 5 analysis.

- Stripe's public testimonial that Fable 5 compressed a 50-million-line Ruby codebase migration that would have taken a team over two months into a single day. This is the kind of named-customer reference that moves enterprise procurement decisions.

By the time WSJ's price-cut story broke on June 11, the strategic question for OpenAI had narrowed: cut prices to retain accounts, or watch the enterprise revenue compress further as Anthropic's pricing-plus-capability advantage compounded.

Comparison table — current API pricing across the frontier (June 2026)

Where the potential OpenAI cuts would land, and where Anthropic sits today.

| Model | Input ($/M tokens) | Output ($/M tokens) | Output ratio | Notes |

|---|---|---|---|---|

| OpenAI GPT-5 | $1.25 | $10.00 | 8x | Already aggressively priced |

| OpenAI GPT-5.5 | $5.00 | $30.00 | 6x | "Frontier" tier; the WSJ story targets cuts likely here |

| OpenAI GPT-5.6 (rumoured Spud) | TBD — reports suggest 2-3x cheaper than Claude Mythos | TBD | TBD | Pretraining completed March 24, 2026 |

| Anthropic Claude Haiku 4.5 | $0.80 | $4.00 | 5x | Cheapest Anthropic tier |

| Anthropic Claude Sonnet 4.5 | $3.00 | $15.00 | 5x | Production default for most workloads |

| Anthropic Claude Opus 4.8 | $15.00 | $75.00 | 5x | Stable behaviour for regulated workflows |

| Anthropic Claude Fable 5 | $10.00 | $50.00 | 5x | Frontier; ships June 9, 2026 |

| Anthropic Claude Mythos 5 | $10.00 | $50.00 | 5x | Restricted access |

| Google Gemini 3.5 Flash | $0.15-0.30 | $0.60-1.20 | 4x | Anchoring the budget tier |

| DeepSeek-V3 | $0.14 | $0.28 | 2x | Open-source-trained, lowest cost |

For a working tool to count tokens and project costs across all of these models side by side, see eCorpIT's free LLM Token Counter at llmtokencounter.ecorpit.com.

What "drastic" might actually look like

Three credible scenarios based on what would meaningfully shift the competitive dynamic:

Scenario A — Across-the-board 30-50% cut on GPT-5.5. Current $5/$30 drops to roughly $2.50-$3.50 input and $15-$21 output. This would put GPT-5.5 at parity with Claude Sonnet 4.5 ($3/$15) on the input side and meaningfully ahead on absolute cost for output. Aggressive but achievable; would significantly compress OpenAI gross margin on the enterprise tier.

Scenario B — Targeted enterprise discounts via volume tiers. Rather than public per-token cuts, OpenAI announces enterprise volume agreements that effectively halve the price for committed-spend customers. Less disruptive to consumer messaging; preserves headline pricing while protecting the largest accounts. The most likely path for an IPO-track company that needs to preserve gross margin optics.

Scenario C — Massive cut on GPT-5 alongside new GPT-5.6 launch. GPT-5 ($1.25/$10) drops to under $1/$5 to anchor the budget tier; GPT-5.6 launches at GPT-5.5's current $5/$30 with materially better benchmarks. This is the cleanest narrative — "we made the older model cheaper while shipping a better new one" — and aligns with the Sam Altman framing of "more value for less spend."

Industry observers and reports suggest GPT-5.6 (codenamed Spud) is positioned with performance approaching Anthropic Mythos at a price 2-3x lower than Anthropic's Mythos-class equivalent. If accurate, the launch would land at approximately $3-$5 input and $15-$25 output — competitive with Claude Sonnet 4.5 on price while approaching Fable 5 on benchmarks. That combination is the most likely public response to the competitive position.

The IPO context — why this matters now

Both OpenAI and Anthropic are preparing for public listings. The price-war dynamics interact with IPO economics in three ways.

Gross margin matters for valuation multiples. Public software companies trade on revenue multiples that depend on gross margin. A price war that compresses gross margin from 75% to 55% would reduce the valuation multiple at IPO. Both companies have reasons to manage cuts carefully.

Customer concentration risk matters for pricing. OpenAI's 1,000+ largest enterprise accounts (and Anthropic's growing 1,000+ million-dollar Claude accounts) are the targets of any price war. Losing high-spend enterprise accounts compresses revenue concentration; winning them improves IPO narrative.

Growth rate matters for storytelling. Anthropic's "$1B to $47B in 15 months" is the cleanest growth narrative in the AI sector. OpenAI's "stable $2B/month run-rate" is solid but lacks the curve. Price cuts that accelerate volume can rebuild the growth narrative for the OpenAI roadshow.

For deeper enterprise AI strategy context, see eCorpIT's generative AI enterprise strategy guide.

What enterprise buyers should expect over the next 60-90 days

Five takeaways for enterprise CIOs and CTOs.

1. Wait before signing long-term OpenAI contracts. If WSJ's reporting is accurate, public pricing changes are likely within weeks rather than months. Locking into 12-month commitments at current rates would be a mistake. Negotiate quarter-by-quarter or push for explicit benefit-of-future-cuts clauses.

2. Anthropic will respond. The WSJ report explicitly notes OpenAI is anticipating Anthropic will make similar moves. The price war is bilateral. Expect Anthropic pricing actions within 30-60 days of any OpenAI cut.

3. Sonnet 4.5 versus GPT-5.5 becomes a closer race. If GPT-5.5 drops to Sonnet 4.5 pricing ($3/$15), the model-selection decision shifts back to capability and reliability for most enterprise workloads. Run benchmark tests on your actual production prompts; do not assume one model is better than the other based on legacy comparisons.

4. The cheap tier (Haiku 4.5, Gemini Flash, DeepSeek) becomes operationally important. Even with frontier cuts, the cheap tier is 5-25x cheaper than the frontier. Tiered routing architectures that use the cheap tier for 60-80% of production traffic continue to win regardless of how the headline price war plays out.

5. Use the eCorpIT Token Counter for actual cost modeling. When prices change, modeling the impact on your specific workload requires counting tokens accurately and applying the new rates. The free LLM Token Counter supports 25+ models side by side with cost projection — when OpenAI announces cuts, the rates will be updated in the tool within a few days.

What founders and growth-stage AI companies should expect

Three additional implications for AI-native companies.

Margin compression on AI-powered products. Many SaaS-AI products price as a 3-5x markup on underlying API cost. As underlying costs fall, customer expectations for pricing fall too. Plan for end-customer price compression in parallel with API cost reduction.

Faster experimentation cycles. Lower per-token costs enable more aggressive A/B testing, more variants in production, and more autonomous agent workflows that previously would not pencil. Companies that can absorb experimentation cost gain compounding advantages.

The end of "use the cheapest model that works." As the gap between cheap and frontier compresses, the optimal architecture often becomes "use the frontier model with tight prompt engineering" rather than "use the cheap model with more careful instructions." The math flips quietly; recompute it quarterly.

India-specific considerations

Three notes for Indian businesses watching this price war.

Indian B2B SaaS companies benefit disproportionately. Indian SaaS companies often run higher AI-feature density per customer than US or European counterparts (because cost-sensitive engineering teams design more aggressive AI workflows). A 30-50% reduction in underlying API costs flows more directly to bottom-line for Indian companies operating at AI-heavy unit economics.

Indian developers face a model-selection question. Indian engineering teams typically have more freedom to experiment across providers than US enterprise teams locked into vendor agreements. The price war is an opportunity to actually run benchmarks on your specific Indian-language and India-specific workloads — particularly because Hindi, Tamil, Bengali, Mandarin and other non-Latin scripts tokenise differently across providers, materially shifting the cost picture.

India's AI infrastructure economics improve. Cheaper LLM access at the API layer reduces the cost of building Indian-language AI products, expanding the practical addressable market for Indian B2C AI applications. For deeper India-specific context, see eCorpIT's cloud cost optimization for Indian companies guide.

FAQ

How eCorpIT can help

eCorpIT builds LLM-aware applications, RAG systems, agentic workflows and enterprise AI integrations for clients across India, the US and the UK. Our work includes model-selection benchmarking on actual production workloads, cost engineering, tiered routing architecture, fine-tuning, prompt design, observability and full production deployment.

If your team needs to navigate the OpenAI vs Anthropic competitive dynamics, plan a model migration, or model the financial impact of upcoming price changes, our engineering team can help. Reach us at ecorpit.com/contact-us/ or contact@ecorpit.com.

References

- Reuters / WSJ (syndication) — "OpenAI Considers Drastic Price Cuts, Anticipating War for Users With Anthropic" via Yahoo Finance: finance.yahoo.com

- US News / Reuters syndication: money.usnews.com

- MarketScreener — same Reuters syndication: marketscreener.com

- InvestingLive — "WSJ: OpenAI weighs major price cuts to compete with Anthropic before IPO push": investinglive.com

- Anthropic — Claude Fable 5 and Mythos 5 launch (June 9, 2026): anthropic.com

- VentureBeat — "Anthropic brings Mythos to the masses with Claude Fable 5": venturebeat.com

- SaaStr — "Anthropic Just Passed OpenAI in Revenue": saastr.com

- Tech Insider — "Anthropic vs OpenAI 2026: 30x Revenue Gap": tech-insider.org

- TradingKey — "Anthropic Revenue Surpasses OpenAI for First Time, IPO as Early as October": tradingkey.com

- Get Panto — Anthropic AI Statistics 2026: getpanto.ai

- Get Panto — OpenAI Statistics 2026: getpanto.ai

- VentureBeat — "Anthropic finally beat OpenAI in business AI adoption": venturebeat.com

- eCorpIT — "Claude Fable 5 + Mythos 5: 80.3% SWE-Bench Pro and a New Tier (2026)": ecorpit.com

- eCorpIT — "LLM Token Counter for 25+ Models (2026)": ecorpit.com

- eCorpIT — "Generative AI Enterprise Strategy 2026": ecorpit.com

- eCorpIT — "Cloud Cost Optimization for Indian Companies 2026": ecorpit.com

Last updated 11 June 2026 by the eCorpIT Editorial team. We will refresh this article when OpenAI publishes actual pricing changes and when Anthropic responds. Revenue and market share figures are accurate as of early June 2026 against publicly available reporting; specific numbers vary across surveys.